Goal Planning - Goal - Part 7

Monitor your goals and the assets associated with that

Monitoring helps you determine exactly when a goal is on track. It provides you a feedback which incorporated allows you to make rectifications and therefore achieve your goals which you have laid out earlier. Feedback is important as it could tell you whether the path that you have chosen to achieve your goals is correct. It is a vindication of some sort. A reality check. It gives you an opportunity to correct your deviations and take you towards your goal.

Till now we have seen :

- Goal Planning - Overview

- Goal Planning - Risk Profile

- Goal Planning - Assets

- Goal Planning - Liabilities

- Goal Planning - Income and Expenses

- Goal Planning - Goals

In my previous article, we talked about creating goals, allocating resources towards goals. These two form the Plan and Do of the P-D-C-A cycle.

How to monitor your goals ?

Goal

Each goal has various assumptions, which needs to be checked on a periodical basis.

You plan to buy a car in in 2025. You have found out the cost of the car is Rs 15,00,000/- and the price of the car would increase by 5% on a yearly basis. You have set the goal in 2020.

Let us look at the assumptions that you have made :

- Cost of the car - Car cost has so many components and it fluctuates on a monthly and yearly basis.

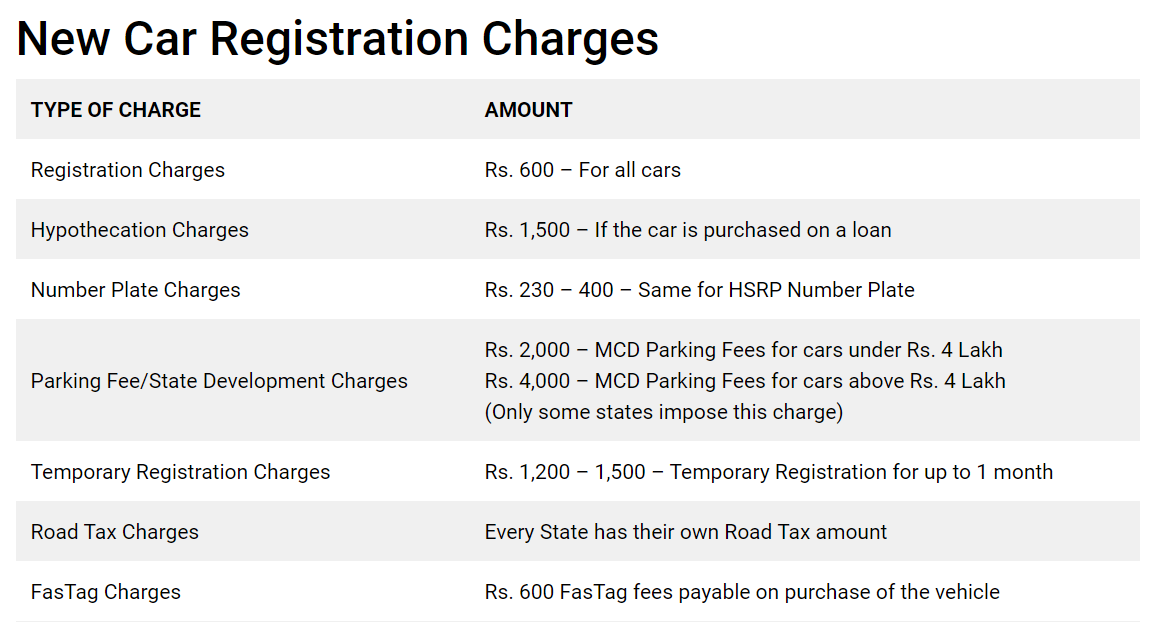

- Taxes - The Government would change taxes periodically as it has a target to meet. Road taxes could be changed, registration charges could be changed, they could introduce green tax

- Inflation - Year on year, prices of raw material would go up and this would eventually be passed on to the customer.

Car Charges - Courtesy - Cars24

- Car Preference - Do you still fancy the same car (roving eye) ? You would not find the same car attractive. As I write now, I see the purchase of Kia cars have caught fancy. People in their 40’s and 50’s would have their first car purchase as Maruti, but the same would not be true for people in their 20’s and 30’s.

Which car would you still like to buy 4 years from now?

Resources associated with goal

You have allocated various resources to your goals. You have assumed that it will give a return of say 10%, however, is it really giving the same on a year-on-year basis ?

Let us take the above goal itself. The purchase of car is within 4 years and therefore you would have associated majority of your resources with debt type assets. You would have assumed that debt type assets would give a return of , let’s say, 8%, but it is actually given 6.5% - you would need to check whether your fund is the best fund in that category. Performance of debt funds are based on various categories including

- fund manager,

- type of funds they have invested,

- prevailing interest rates,

- fund category - fund duration

- Yield-To-Maturity etc…

Moreover, in debt funds, it is not a wise idea to take more risk as the safety of the funds is of paramount importance.

In case of a long term goal, you would have heavily invested in equity funds, in such case, you would want to check whether you are nearing your goal(say 2 - 3 years away). If yes, would this be the right time to switch to debt funds ?

In summary , you need to check whether your mutual fund (equity or debt) will give you the return that will help you achieve the goal.

In case the return of your fund is nearly the same as that of your best performing funds, you would need to allocate more funds so that you can meet your goal .

Conclusion

This concludes my 7 part series on Goal Planning. Hope you found it useful and wish you all the best in case you have set your goal and on the right track to achieve your goal. If you would need some help don’t hesistate to drop a line to me

References